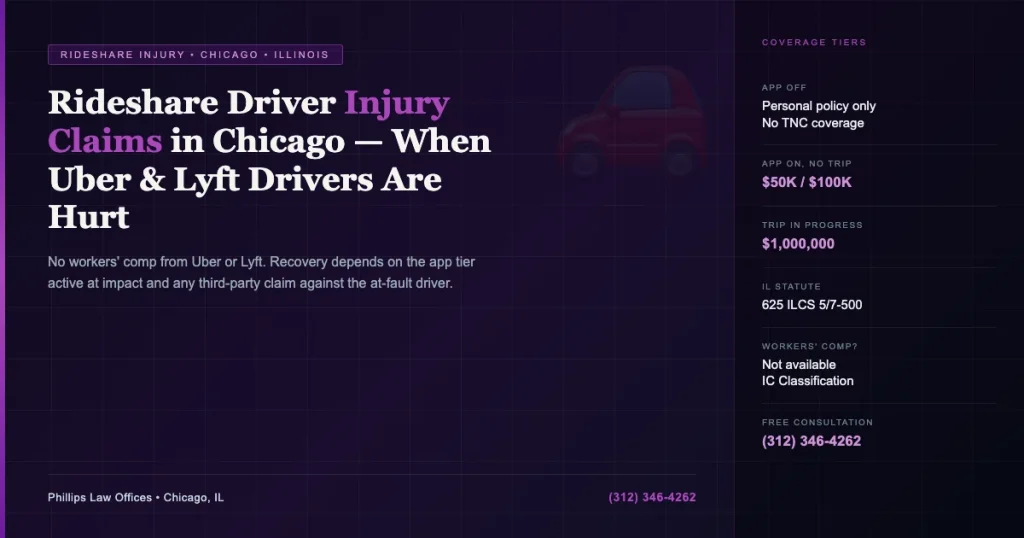

Short answer: Uber and Lyft classify their drivers as independent contractors, not employees, which means injured rideshare drivers have no access to workers’ compensation from the company. Recovery after an on-the-job crash comes from two sources: the TNC’s commercial insurance tiers (which vary depending on whether the app was on and whether a trip was active) and any third-party liability claim against the at-fault driver. Understanding which tier applies to your specific moment of injury is the key to knowing what you can recover.

The independent contractor classification is one of the most consequential legal fictions in the gig economy. I hear it described as a gap by clients who were driving for Uber or Lyft when they were hurt, but in practice it is more accurate to describe it as a design feature. The structure that prevents drivers from accessing workers’ comp is not accidental. It is built into the business model. What it means for you, practically, is that your path to recovery runs through the commercial insurance tiers, your own coverage, and any fault-based claim against whoever caused the crash.

Independent Contractor vs. Employee: Why It Matters

In Illinois, employees injured on the job have access to workers’ compensation benefits regardless of fault. Medical bills, a portion of lost wages, and rehabilitation costs are all covered through the employer’s workers’ comp policy. That system does not apply to independent contractors.

Uber and Lyft have consistently maintained in Illinois courts and regulatory proceedings that their drivers are independent contractors, not employees. While that classification is being challenged in various states, Illinois law as currently applied does not treat rideshare drivers as employees for workers’ compensation purposes. The consequence is that if you are hurt while driving for Uber or Lyft, you cannot file a workers’ comp claim against the company. You are left to pursue recovery through other channels.

This is not a minor distinction. Workers’ compensation provides no-fault coverage. The commercial insurance tier system that applies to rideshare drivers is fault-based, meaning your recovery depends on proving who caused the accident and what their insurance covers at the exact moment of your injury.

Uber and Lyft Insurance Coverage for Drivers

Both Uber and Lyft maintain commercial auto insurance that covers drivers, but the coverage is structured in tiers based on the status of the app and whether a trip was in progress at the moment of the crash. The tiers are not equivalent, and the distinction between them can mean the difference between $50,000 and $1,000,000 in available coverage.

| App Status | Uber Coverage (Driver) | Lyft Coverage (Driver) |

|---|---|---|

| App off (personal use) | None, personal auto policy only | None, personal auto policy only |

| App on, no trip accepted | $50,000/person, $100,000/accident, $25,000 property; contingent comprehensive/collision | $50,000/person, $100,000/accident, $25,000 property; contingent comprehensive/collision |

| Trip accepted or in progress | $1,000,000 third-party liability; uninsured/underinsured motorist; contingent comprehensive/collision ($1,000 deductible) | $1,000,000 third-party liability; uninsured/underinsured motorist; contingent comprehensive/collision ($2,500 deductible) |

The tier you fall into is determined by a timestamp logged in the app at the exact moment of the crash. Uber and Lyft both have records of this. In disputed cases, that data becomes a central issue in the claim.

When the App Is On vs. Off: Coverage Tiers Explained

If your app was completely off at the time of the accident, you were using your vehicle as a private driver. Uber and Lyft owe you nothing. Your personal auto policy is the only coverage that applies, and standard personal auto policies often exclude commercial use. This means you may be driving without any effective coverage during personal time if your insurer knows you drive for a TNC and your policy has not been updated accordingly.

If the app was on but you had not yet accepted a ride request, the intermediate tier applies. Uber and Lyft both provide $50,000 per person and $100,000 per accident in third-party liability coverage during this period. This is substantially higher than Illinois’s mandatory minimums but far below the full commercial policy that activates once a trip begins.

Once you have accepted a trip request and are en route to pick up a passenger, or are actively transporting a passenger, the full $1,000,000 commercial policy is in effect. This is the tier that provides the most meaningful coverage for serious injuries.

Third-Party Claims Against the At-Fault Driver

The TNC insurance tiers described above cover claims against the TNC’s policy, but if another driver caused your accident, you also have a separate fault-based claim against that driver and their insurer. This is a third-party claim, and it operates independently of the TNC coverage.

If the at-fault driver is underinsured, the TNC’s uninsured/underinsured motorist coverage (available during active trips) may provide additional recovery. Stacking these coverages requires careful coordination to avoid subrogation pitfalls and ensure you are not inadvertently waiving rights against one insurer while pursuing another.

The third-party claim is often the most important source of recovery in driver injury cases. It requires proving the other driver’s negligence, documenting your injuries, and negotiating with their insurer or filing suit. This process is identical to any other Illinois car accident claim, with the added complexity of coordinating with TNC coverage.

Attorney insight: The independent contractor classification that denies rideshare drivers workers’ comp benefits is being actively challenged in California, Massachusetts, and other states. In Illinois today, however, the classification stands, and injured rideshare drivers must work within the TNC commercial coverage tiers and fault-based third-party claims. The good news is that when a trip was in progress, the $1,000,000 commercial policy provides substantial room for recovery in serious injury cases. The challenge is coordinating those claims without inadvertently compromising your rights.

Illinois Law on TNC Coverage

Illinois regulates Transportation Network Companies under 625 ILCS 5/7-500 et seq., the Transportation Network Providers Act. This statute establishes the insurance requirements that Uber, Lyft, and other TNCs operating in Illinois must meet. The law mandates the tiered coverage structure described above and requires TNCs to maintain primary liability coverage when a driver is logged into the app.

The Illinois Insurance Code at 215 ILCS 5/ also applies to how commercial insurers are required to process and respond to claims under these commercial policies. Knowing both the TNC-specific statute and the general insurance code provisions helps identify when an insurer is acting in bad faith or improperly delaying your claim.

Illinois also requires that TNC commercial coverage be primary, meaning it applies before any personal auto policy the driver carries. This matters because some personal auto insurers have tried to disclaim coverage based on commercial use exclusions, then argued that their policy should apply anyway when it benefits the insurer. The statute resolves this by establishing the priority of coverage clearly.

Steps After Being Injured as a Rideshare Driver

The steps you take immediately after being hurt while driving for Uber or Lyft affect your ability to recover. Here is what matters most in the immediate aftermath and in the days that follow.

- Document the app status at the time of the crash. Take a screenshot if possible, or note the trip details before the session closes. The app status at the exact moment of impact determines which coverage tier applies.

- Report the accident through the Uber or Lyft app as required by their driver agreements. Failure to report through the proper channel can complicate the claim process later.

- Get medical attention immediately, even if injuries seem minor. Rideshare driving involves repetitive use of your vehicle and physical vulnerability in traffic. Soft tissue injuries and whiplash can become serious over days.

- Document the scene. Photograph the vehicles, the intersection, any road conditions, and the other driver’s information and insurance card.

- Notify your personal auto insurer, but do not make a recorded statement to any insurance company before consulting an attorney.

- Preserve all records related to your driving activity, including trip logs, earnings records, and any communications from Uber or Lyft related to the accident.

Frequently Asked Questions

Does Uber or Lyft provide workers’ compensation for drivers?

No. Uber and Lyft classify their drivers as independent contractors rather than employees. In Illinois, workers’ compensation benefits are available only to employees. Because rideshare drivers are not treated as employees under current Illinois law, they have no access to workers’ compensation through Uber or Lyft. Recovery after a crash must come from the TNC’s commercial insurance tiers and any third-party claim against the at-fault driver.

What if I was injured and the app was off at the time?

If the Uber or Lyft app was completely off when the accident occurred, you were using your vehicle as a private driver and neither TNC owes you any coverage. Your personal auto policy is your only source of coverage for that accident. Be aware that many standard personal auto policies contain commercial use exclusions, so if you regularly drive for a TNC, you should verify that your personal policy covers you during non-app time.

Can I sue Uber or Lyft directly for my injuries?

Direct negligence claims against Uber or Lyft as corporations are difficult but not impossible. Because they maintain the independent contractor classification, they are generally not vicariously liable for driver negligence under respondeat superior. However, claims based on the company’s own negligence, such as failure to screen drivers, failure to maintain adequate insurance, or knowing placement of an unfit driver, may be viable in specific circumstances. An attorney can assess whether a direct claim against the TNC is appropriate based on the facts of your case.

What coverage applies between trips when the app is on?

When you are logged into the Uber or Lyft app but have not yet accepted a ride request, the intermediate coverage tier applies. Both TNCs provide $50,000 per person and $100,000 per accident in third-party liability coverage, plus $25,000 for property damage, during this “app on, no trip” period. This is substantially more than Illinois’s statutory minimums but significantly less than the $1,000,000 commercial policy that activates when a trip is accepted or in progress.

Do I need my own commercial auto policy as a rideshare driver?

Many insurance professionals recommend that rideshare drivers carry a rideshare endorsement on their personal auto policy or purchase a standalone commercial policy. Standard personal auto policies often exclude commercial use, which creates a gap in coverage during the intermediate tier period or when the app is off. A rideshare endorsement fills that gap at relatively low additional cost. Some insurers also offer policies specifically designed for TNC drivers that coordinate with the Uber or Lyft commercial coverage tiers.

Authoritative Sources

- 625 ILCS 5/7-500 et seq., Illinois Transportation Network Providers Act (TNC insurance requirements and driver coverage obligations)

- 215 ILCS 5/, Illinois Insurance Code (insurer obligations and commercial policy requirements)

Related Illinois Injury Guides

- Rideshare Passenger Injury Claims in Chicago

- Food Delivery Driver Accidents in Chicago

- Medical Liens in Chicago Auto Accident Cases

- Loss of Future Earnings in Illinois Injury Cases

If you were injured while driving for Uber or Lyft in Chicago, the Phillips Law Offices team can help you understand which coverage tiers apply, coordinate claims across multiple insurers, and build a full picture of your available recovery. Call us at (312) 346-4262 for a free consultation.